In last week's article, we examined the role that salary plays within a profit extraction strategy and the advantages and disadvantages of remunerating directors through PAYE.

This week, we turn to what is often considered the most popular profit extraction method for owner-managed businesses: dividends.

Many business owners have heard that dividends are more tax-efficient than salary. Whilst this can be true in certain circumstances, the reality is more nuanced. Dividends are governed by company law requirements, can only be paid under specific conditions, and should form part of a broader remuneration strategy rather than being viewed in isolation.

In this article, we explore how dividends work, when they can be paid, the tax treatment of dividend income, and the common mistakes that business owners should avoid.

A dividend is a distribution of profits made by a company to its shareholders. Unlike salary, a dividend is not paid in return for services performed. Instead, it represents a return on the shareholder's investment in the company.

This distinction is important because it means that only shareholders can receive dividends. A director who is not also a shareholder cannot receive dividends from the company. Similarly, the amount of dividends paid generally depends on the shareholder's ownership rights rather than the work they perform within the business.

One of the most common misconceptions about dividends is that a company can declare them whenever it has money in the bank. This is not the case. Under UK company law, dividends can only be paid out of distributable profits.

Section 830 of the Companies Act 2006 defines distributable profits as a company's accumulated realised profits, less its accumulated realised losses. In simple terms, a company must have generated sufficient profits, after taking account of previous distributions and losses, before it can lawfully pay a dividend.

The key point is that cash and distributable profits are not the same thing. A company may have substantial cash reserves but still be unable to pay a dividend because it does not have sufficient distributable profits. Equally, a company may have adequate distributable reserves on paper but lack the cash flow necessary to make a distribution. Both the accounting position and the company's liquidity must therefore be considered.

Before declaring a dividend, directors should ensure that:

Failure to comply with these requirements may result in an unlawful dividend, the consequences of which are discussed later in this article.

It is worth understanding the distinction between interim dividends and final dividends, as the two follow different procedures.

An interim dividend is one declared by the directors during the financial year, typically by board resolution, without requiring shareholder approval. This gives directors flexibility to distribute profits as they arise throughout the year.

A final dividend is one recommended by the directors and declared by the shareholders, usually at the annual general meeting or by written resolution. Once declared, a final dividend becomes a debt owed by the company to its shareholders.

For most owner-managed businesses where the directors and shareholders are the same individuals, the distinction may appear largely procedural. However, following the correct process for each type of dividend is important for maintaining proper corporate governance and reducing the risk of challenge.

Dividends have traditionally been a popular profit extraction method because they are not subject to National Insurance Contributions. This can create significant savings compared to extracting the same amount through salary.

To illustrate, consider an owner-manager who wishes to extract an additional £10,000 from the company. If taken as salary, the company would pay employer's National Insurance on that amount, and the individual would pay employee's National Insurance in addition to income tax. If taken as a dividend, neither employer's nor employee's National Insurance would apply. At current rates, the combined employer's and employee's National Insurance saving on a £10,000 extraction could amount to several thousand pounds, depending on the individual's earnings level and the applicable NIC thresholds. The saving becomes increasingly material as extraction amounts increase.

Beyond the National Insurance advantage, dividends offer flexibility. Unlike salaries, which are often paid monthly, dividends can be declared at different times throughout the year depending on the company's profitability and cash flow requirements. This allows directors and shareholders to adapt their remuneration strategy as circumstances change.

Although dividends are not subject to National Insurance Contributions, they are still taxable income. Shareholders must generally declare dividend income through their Self Assessment tax returns where required.

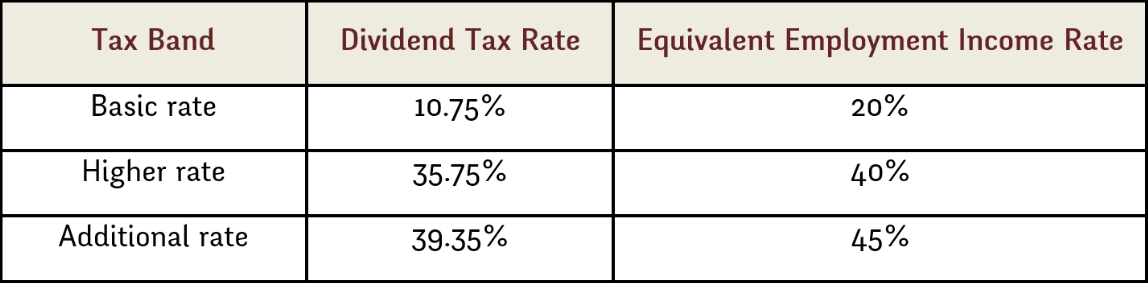

Dividend income is subject to its own tax regime, which differs from employment income. Each tax year, individuals benefit from a dividend allowance, which permits a certain amount of dividend income to be received free of tax. The dividend allowance currently stands at £500 per year.

Dividend income falling above this allowance is taxed at the following rates:

These rates apply for the 2026/27 tax year and remain lower than the equivalent rates for employment income, which is one of the reasons dividends are considered tax-efficient. However, business owners should ensure they are working with current figures rather than relying on historical assumptions, as rates and allowances are subject to change.

The applicable rate will depend on the individual's total taxable income, the amount of dividend income received, and the interaction between dividend income and other sources of income. As a result, the tax position can vary significantly between shareholders. What may be highly tax-efficient for one individual may produce a very different outcome for another.

A common question business owners ask is whether they should take a salary or dividends. The answer is rarely one or the other exclusively.

The most effective remuneration strategies often involve a carefully planned combination of both. Salary provides Corporation Tax relief and may assist with State Pension entitlement and borrowing applications. Dividends may reduce National Insurance costs and provide greater flexibility. The objective is typically to balance these advantages in a way that reflects the individual's circumstances and the company's objectives.

A strategy focused entirely on dividends may not always produce the best outcome, particularly where pension planning, mortgage applications, or future business growth are important considerations.

Dividends can also play an important role in family-owned businesses. Where family members hold shares, dividend payments may allow profits to be distributed across multiple shareholders, potentially making use of each individual's personal allowance, dividend allowance, and lower tax bands.

However, ownership structures should be carefully reviewed before implementing any such planning strategy. Directors should ensure that shareholdings accurately reflect the intended ownership arrangements, that any changes are properly documented, that company law requirements are satisfied, and that the tax implications are fully understood before action is taken.

Despite their popularity, dividends are often an area where mistakes occur. Some of the most common issues are set out below.

One of the most common mistakes made by owner-managed companies is declaring dividends without first confirming that sufficient distributable reserves exist. Doing so can result in an unlawful dividend.

Where a shareholder knew, or had reasonable grounds for believing, that the distribution was unlawful, they may be required to repay the amount received to the company. In owner-managed businesses, where the directors and shareholders are often the same individuals, it can be particularly difficult to argue that they were unaware of the company's financial position or the lack of available reserves.

The consequences of an unlawful dividend can therefore be significant, giving rise to both financial and legal liabilities.

Dividend decisions should be supported by appropriate corporate documentation. Directors should maintain dividend vouchers for each payment, minutes of the directors' meeting or written resolution authorising the dividend, management accounts supporting the declaration, and accurate accounting records. Poor documentation may lead to difficulties if HMRC raises questions regarding the payments and may also make it harder for the company to demonstrate compliance with the Companies Act requirements.

Many owner-managed businesses operate informally, with directors withdrawing funds throughout the year. Unless properly documented as dividends, these withdrawals may constitute loans from the company to the director. This distinction can have significant tax consequences, including potential liability under section 455 of the Corporation Tax Act 2010 and a benefit in kind charge on the director. We will examine Director's Loan Accounts in greater detail later in this series.

Tax legislation changes regularly. The dividend allowance has been reduced considerably over recent years, and rates of dividend tax have also increased. Whilst dividends continue to provide advantages in many situations, they should not automatically be assumed to be the most efficient extraction method. Each business owner's circumstances should be reviewed individually and revisited periodically to ensure the chosen strategy remains appropriate.

As with salary planning, dividends should not be considered solely from a tax perspective. Business owners should also consider their future pension planning requirements, mortgage and lending needs, succession planning, shareholder relationships, future investment requirements, business growth objectives, and any potential sale of the business.

A dividend strategy that appears attractive today may not align with longer-term commercial objectives. For example, a business owner planning to sell the company within the next few years may wish to retain profits within the business to support its valuation, rather than extracting them by way of dividend. Similarly, an individual seeking mortgage finance may find that lenders place greater weight on salary income than dividend income, which could influence the balance of the remuneration strategy.

Dividend planning sits at the intersection of company law and tax law. Before declaring dividends, directors should ensure that the company has sufficient distributable profits and that the proposed extraction strategy aligns with their broader financial goals.

Professional advice can help business owners avoid common pitfalls, remain compliant with legal requirements, and develop a remuneration structure that balances tax efficiency with commercial practicality. Given the interaction between the Companies Act, income tax legislation, National Insurance rules, and the settlements provisions, this is an area where tailored guidance can add considerable value.

Dividends remain one of the most widely used methods of extracting profits from owner-managed businesses. They offer flexibility, can reduce National Insurance costs, and often form an important component of a tax-efficient remuneration strategy.

However, dividends are not simply a substitute for salary. They can only be paid from distributable profits, must comply with both tax and company law requirements, and carry real consequences where the rules are not followed. For many business owners, the most effective approach is a carefully structured combination of salary, dividends, and other extraction methods tailored to their individual circumstances.

In the next article of our Profit Extraction Series, we will examine how employer pension contributions can be used as a highly tax-efficient method of extracting value from a company while simultaneously supporting long-term retirement planning. Pension contributions interact directly with the salary and dividend decisions discussed in these first two articles, and understanding how all three elements work together is essential to building a robust remuneration strategy.